Post-Brexit Property Buying Offers Once-in-a-Generation Opportunity

Share News:

We live in a world of Chicken Littles, whereby the reactions to the slightest events become magnified to outlandish and irrational proportions.

Mass shooting? Buy a gun.

On June 23, the UK voted to leave the European Union and the world has barely taken a breath from all the crazy it unleashed. Me? I take breaths. Reflexive panic is when mistakes happen.

Of course, there were different strategies needed for buying and selling real estate during the global recession. Regardless, panic served none well.

Sure there is opportunity outfoxing an ill-informed, reactionary mob, but within the topic of UK real estate, it’s doubtful any of us had a suitcase full of dollars ready to chuck at a property on June 24.

For the purposes of real estate, I’ll not comment on Brex-regret, hollow promises, and the current realities “Leave-ers” downplayed as inflated propaganda. Nor will I comment on “Leave” leaders now running for the door, including campaign ringmaster Nigel Farage. They’ve chosen to “leave” their mess to others, being termed “rats off a sinking ship.”

As a second home buyer, there are only three indicators to be concerned with: property values, currency exchange rates, and mortgage interest rates. While currency and interest rates fluctuate by the second, property values are a slower, and in this case, more important target.

All the other tables, graphs, and doom-saying are a distraction. As an American, you don’t have a personal stake in the free movement of people and goods through the EU – a cornerstone of EU membership. Americans stood in the long Customs line before and we’ll continue to do so. Sure, more constrained trading policies may inflate the cost of some goods over time, but if you’ve got enough dosh to buy property in the UK, an extra 50p per kilo of bananas isn’t going to sting too badly.

Property Values

Future bargain? Across the street from The Ritz for £17.5 million.

It’s really too soon to tell how this will play out long-term. The London property market, after decades of non-stop appreciation, was already showing signs of decline in the months prior to Brexit. In addition to Brexit fears, a new tax on investment properties as well as rumblings out of Whitehall to expose shell company owners added to the declines. As one would expect, outside London, the effect was less pronounced.

In anticipation of the vote, estate agents report that June property transactions surged, along with currency rates, as polls showed the “Remain” camp leading. Obviously it’s too soon for actual data on volumes and prices to be reported. Anecdotally, many estate agents are standing on proverbial rooftop ledges. Playing out like the currency market in slow motion, when official numbers are available, what will be seen first are the the reactions of those who panicked first.

For those with speculative bones, Edinburgh, Scotland, or Dublin, Ireland, may be worth some research. If Article 50 is invoked and Scotland votes to leave the UK and rejoin the EU, the backbone of London’s financial services industry may relocate to language-friendly Scotland or already-in-the-EU Dublin.

One thing is certain in the short-term: already-built London property developments targeting foreign buyers will continue their price slide. Planned developments will be mothballed. In fact, stocks of developers have fallen hardest post-Brexit. Stocks prices for the UK’s largest home builders have dropped 30 percent since the vote. As of this writing three of the largest commercial property funds have stopped trading as investors seek to cash out from operations without the liquid assets to cover.

This gives UK natives access to properties that were overpriced for the local market. The same can be said of wealthy areas of traditional London, such as Mayfair, Belgravia, and Knightsbridge, as well as areas catering to European ex-pats who may feel xenophobia’s rise and continued employment in the UK is less secure.

Longer-term, buyers need a good estate agent and to keep an eye on the property market. Just like the US recession cratered prices, the smart buyer looked at high-water marks to judge where valuations would someday return to. The key to property buying post-Brexit is to focus on the delta between current and pre-Brexit prices. The bigger the gap, the bigger the opportunity.

This will take time to track, but time is on the buyer’s side. With approximately half of London’s residences being used as investments and those owners being precisely the ones who will run away, opportunity abounds for the patient. Remember your recent history: when the US housing market began crashing in 2008, the smart buyer didn’t rush in — they waited.

Currency Exchange Rates

1-year: Pound against the dollar

The second the results were announced, the Pound dropped to a low of ~$1.32 against the dollar. News outlets made hay of the fact that such a huge drop hadn’t been seen in decades. What was conveniently left out (because it wasn’t as panic-inducing) was that in the run-up to the vote, the Pound had gained about 8 cents against the dollar. The real drop was closer to a dime versus the widely quoted hysteria. Bad, but not as bad.

In fact for all of 2016, the Pound averaged in the low-mid $1.40s with a low of $1.38 in February and a high of $1.47 in April against the dollar.

For reference, the Pound has been dropping against the dollar for two years. In June 2014, the Pound was trading in the $1.60s hitting a high of ~$1.70, by June 2015 it had fallen to mid-$1.50s.

Every penny of exchange rate change equals $1,000 per $100,000 spent. So for every $100,000 spent on a UK home in June 2014, you’ve lost $37,000. Ouch! Pre-Brexit you’d only lost $20,000-ish. Note, property values in the past two years have grown precipitously, largely offsetting the pre-Brexit currency losses.

Add to that the continued drop in currency rates, currently sub-$1.30 with some banks setting a landing at $1.20 to the Pound. How bad would you feel had you converted quickly after the June 23rd vote? Patience.

The Pound is not finished gyrating. There will be several opportunities in the coming months and years to capitalize on a cheaper Pound. Watch for other shocks to the system that will trigger panicking sellers.

With a future looking like property and currency values are heading south, finding the bottom of both will be tricky. A buyer must balance both property potential against currency devaluations.

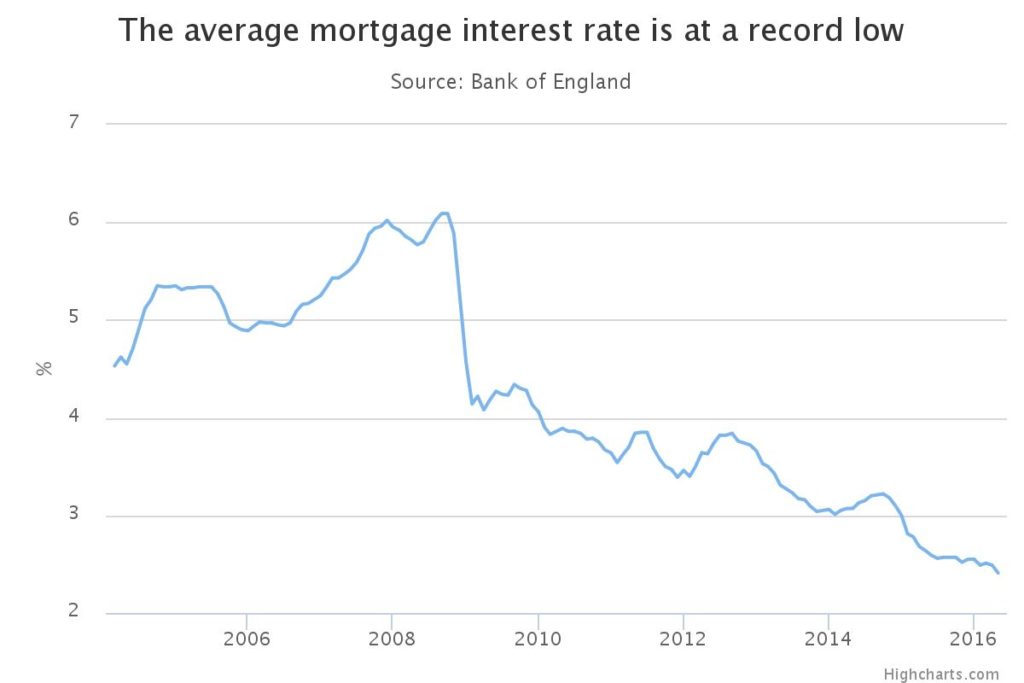

Mortgage Interest Rates

Pre-Brexit UK Mortgage Rates

The third part of this equation is the cost of money. Reporters are pointing to an expectation of raising interest rates after a long period of decline. Official post-Brexit measurements are not available, but scoping out a few UK banks I see slight rate declines for a 10-year fixed mortgage. What the Bank of England reported at an average 3.15 percent in June can now be found for ~3 percent. Of course with all mortgage rates, there are various buy-downs, points, etc. that impact a rate.

Note: The UK does not offer 15- and 30-year fixed mortgages. In addition to variable rate mortgages, they have fixed-rate options ranging from 2-10 years before refinancing.

If a buyer would require a UK mortgage, interest rates matter. But a significant portion of buyers pay cash. Those without the actual cash may choose to remortgage a US property at our more attractive and longer-term rates to facilitate an all-cash buy.

Only Fools Rush In

Smart investors rush in when Fools rush out

It’s important to understand that Brexit reactions will be a series of stair steps. It’s not one reaction and everyone will just move on. The markets will find their feet in the coming months as the early panickers work their way through the system.

Next there will be another drop when the UK actually invokes Article 50, the formal notification of an intent to leave the EU. That will send more towards the exit. Many in the “Remain” camp are holding out hope the government won’t act on the referendum. One candidate for Prime Minister has signaled she’d wait until 2017 to start the process. Of course she’s the same one who wants a lot of immigrant residents kicked out (which would have a disastrous effect on real estate prices),

As negotiations drag on (Article 50 gives two years for a complete separation), various headlines will influence markets lower. The big kicker is the free movement of people and goods. If/when the UK and Europe decide that’s a deal-breaker, there will be another falter. High-level business relocations will also shock the indexes lower.

If Scotland, who voted to remain in the EU, approves their assumed second vote to leave the UK with the goal of remaining in the EU, that will send a further shockwave. Were financial services firms to decamp from London and setup shop in Edinburgh or Dublin, the effect would be magnified.

As a potential property buyer, timing is everything. In the case of Brexit, the best opportunities will only become visible with patience. Real estate gets cheaper with every “Chicken Little” moment.

For those always wanting a home in London, this may be a once-in-a-generation opportunity if you play it right.

Remember: When I’m not stirring up trouble in Dallas, Texas or Honolulu, Hawaii for Candysdirt.com and SecondShelters.com, I’m off scouting interesting locations for a second home. In 2016, my writing was recognized with Bronze and Silver awards from the National Association of Real Estate Editors. If you’re a Realtor with second home clients who’d like me to feature their journey, shoot me an email sharewithjon@candysdirt.com

4 Comments

Had dinner with a well-traveled New Yorker last week who told me European friends say Brexit will make it more difficult for Europeans to travel from say, the UK to Spain. In the states we tend to forget how easy we have it travel wise, no border crossings between Texas and Arkansas. Just a welcome sign. Brexit is going to change that, she says.

It may. It all depends on how the Brexit terms are negotiated. An overwhelming majority from both the Leave and Remain camps are for the free movement of Brits and EU citizens. The vote was more about keeping refugees out (something the Leave campaign NOW admits is unlikely even though they campaigned on that messsage).

As of today, all major property investment trusts have halted trading and some believe it will last at least through the end of 2016. The afraid are hurting themselves on the way out. The more who force asset sales to generate cash will over saturate the commercial property market which will in turn continue to drive down prices. This is what self-cannibalization, the ugly side of “supply and demand,” looks like.

While not mentioned in the above piece, the commonly acknowledged root cause for the astronomical ascent of

London residential values is the fact that the UK made a strategic decision to not tax the non-UK earnings of its residents.

While there are many places among the 24 time zones that fortunes can be made, in a great deal of them, one literally takes his/her life in their hands by residing there. As one who did extensive due diligence on an extremely lucrative project on a commodity from Russia in great demand for the qualities available only from there, I will assure you that one who is aware of the risks of establishing a lucrative business in Russia will chose to pass on the opportunity. Being a deceased billionaire is not an attractive scenario. Also, we discovered that a common business practice in Russia is to have a competitor thrown into prison. As the Russian prisons are rampant with tuberculosis, that equals a death sentence.

I suggest that the manipulative Brexit vote was a colossal mistake that could result in an enormous exit of capital from the UK, but Scotland has never had such a lucrative opportunity to leapfrog its former compatriots

as it has now.

Those who bought homes in London anytime in the past two years will have difficulty recovering from that choice, just as anyone who makes a major investment in the US probably will suffer if weird things occur and those who are drawn to charismatics turn out in droves resulting in the unconsciously incompetent Donald J. Trump being elected as POTUS in a time in which the 45th President may well be called upon to nominate three separate Associate Justices to the United States Supreme Court. These could still be serving through 2050.

With the baggage carried by the presumptive Democratic nominee, it could happen.